Memorandum for President Trump on a National Robotics Strategy

Subject: AI and Robotics Power: Securing America’s Future

Purpose: Secure U.S. Leadership at the Convergence of AI and Robotics

Objectives:

- Set national-level technology goals for robotics that ensure U.S. leadership in development, deployment, and responsible use, driving economic growth, enhancing national security, and improving quality of life.

- Accelerate the adoption of robotics and embodied AI across U.S. industries to enhance competitiveness and strengthen the American workforce.

- Achieve strategic independence for the U.S. robotics industry, ensuring a resilient domestic ecosystem capable of leading innovation, production, and deployment without undue reliance on any country of concern, especially China.

Background

Recent AI advances have opened the door for general-purpose robotic systems that can reason and plan. Once deployed, these systems will drive productivity gains across many fields, including advanced manufacturing “factories of the future,” AI-enabled self-driving labs, logistics facilities, smart agriculture, and space exploration. Since deploying robotics boosts productivity, accelerating adoption is a vital part of a pro-growth agenda. Deploying robots also offers the United States a way out of the severe labor shortage it faces across a variety of sectors. For example, the United States faces a projected shortage of 2.1 million manufacturing workers by 2030.[1] Today, robots can augment human labor by performing dull, dirty, or dangerous tasks.

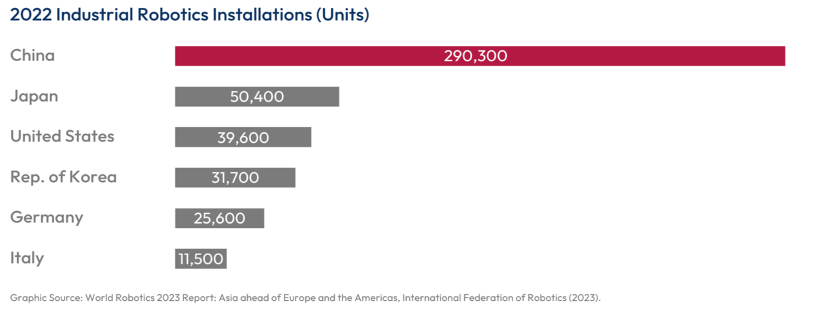

While the United States maintains an edge in robotics software and AI, global leadership hinges on overcoming its weaknesses in hardware commercialization, scaling, and adoption. China adopted more industrial robots than the rest of the world in 2023 and has announced its intent to lead the world in humanoid robotics by 2027.[2] Meanwhile, U.S. firms face obstacles to adoption, including a fragmented regulatory environment. Without rapid action, the nation could become reliant on China for robotics hardware and components, similar to its position in the commercial drone and electric vehicle markets.

Recommendations

Objective 1: Set National-Level Technology Goals for Robotics

- Develop a National Strategy for Robotics Commercialization. Beijing has rolled out a series of national-level robotics strategies, which include R&D goals, financial incentives, and adoption quotas. The United States has no strategy. Coordinated national policy efforts to encourage robotics adoption are necessary, including streamlining the regulatory environment and instituting a common-sense licensing system for trusted systems. The White House should lead the development of a National Robotics Strategy and implementation plans to increase robot adoption across key mission areas, particularly manufacturing, autonomous vehicles, agriculture, and energy.

- Scale Factories of the Future to Rebuild the Defense Industrial Base. To offset China’s manufacturing dominance, the U.S. Department of Defense (DoD) should create a network of scalable, AI-enabled factories that can adaptively produce goods.[3] In addition to boosting the U.S. manufacturing base in peacetime for industries such as automotive, a network of scalable factories would create essential industrial surge capacity in the event of a conflict. The DoD should establish a national program office to track these facilities and drive adoption.

- Launch a Made in America Robotics Initiative. Without a clear market signal from the government, the nation risks becoming dependent on China for robotics hardware and components, as it has for commercial drones.[4] The United States should aim to build several clusters of robotics production across the nation by catalyzing private investment across the robotics supply chain.[5] Attracting additional foreign direct investment from robotics firms in like-minded countries such as Japan, South Korea, and Germany should be a priority. The United States should consider financial incentives, like tax credits for robotics and key components production, as well as targeted grants and loan programs through the Department of Commerce.

Objective 2: Accelerate Robotics Adoption Across Industries

- Create a Data Foundry for Robotics and Industrial AI. Unlike earlier families of AI models–including both computer vision and LLMs–no Internet-scale database exists to train embodied AI systems. Training embodied AI systems requires real-world physical data, including where objects are located spatially, how they move and interact, and processes to manipulate them. Because China can compel firms to share their data, it has a major advantage over the United States in training industrial AI. To compete, the United States must create a trusted third-party hub that works to collate and distribute private-sector industrial datasets for mutual benefit.[6] A tiered access data foundry would incentivize pre-commercial sharing of industrial data and could be linked to the recently announced AI for Resilient Manufacturing Institute, the newest of the Manufacturing USA Institutes.

- Leverage Tax Policy to Drive Adoption. Tax credits and other fiscal incentives can accelerate robotics adoption across U.S. industries by reducing the high upfront capital costs that often deter businesses, particularly small and medium-sized enterprises, from investing in automation. Compared to other industrialized nations, the U.S. tax code does not adequately incentivize capital investment in equipment and manufacturing software.

- Accelerate Robotics Adoption for Main Street. Small and Medium-sized Manufacturers (SMMs) make up 98% of the U.S. industrial base, but these firms lag far behind in terms of adopting advanced manufacturing technologies.[7] Across the U.S. industrial base overall, for example, only 12% of U.S. factories overall utilize robotic automation.[8] Many SMMs cite a lack of access to capital as the key barrier to adoption. The United States should expand capital access programs to accelerate the adoption of robotic systems among SMMs, while also providing matching funds to state-level grant programs that support adoption.[9]

- Position the American Workforce for the Robotics Age. The frontline workers of the future will require training to adapt to emerging human-machine paradigms presented by the introduction of robotic systems into production environments.[10] The United States currently spends only 0.1% of GDP on active labor-market programs, less than the OECD average of 0.6%.[11] The United States should scale successful workforce programs, such as that established by the Advanced Robotics for Manufacturing (ARM) Institute, the nation’s leading public-private partnership dedicated to advanced innovation in AI and robotics, which maintains a unified platform for connecting job-seekers with education programs to develop skills in robotics.[12]

Objective 3: Secure Independent U.S. Leadership in Robotics

- Prevent Chinese Firms from Dominating the Robotics Stack. Robotic systems are packed with a variety of sensors and networking components that present significant threat vectors if produced by foreign adversaries. These systems are often deployed around critical infrastructure and, when produced by adversarial nations, increase America’s exposure to threats of data exfiltration and remote sabotage or manipulation of critical systems.[13] Executive Branch authorities established during the first Trump administration and leveraged during the Biden administration should be used to address this national security threat. The Bureau of Industry and Security at the Department of Commerce should use its Information and Communication Technology & Services (ICTS) supply chain authorities to restrict robotics components from China and other countries of concern.[14]

- Build a Strategic and Integrated Robotics Market with Allied Nations. Blocking Chinese robotics companies from the U.S. market will be ineffective unless other market economies take similar steps. To create a sufficiently large market where countries that play by the rules can compete fairly, America should persuade other allied nations to adopt similar protective measures. In addition to negotiating market access for U.S. players, the Executive Branch can ensure interoperability between nations by prioritizing standards development.

The State Department, Office of the U.S. Trade Representative, and Department of Commerce should pursue targeted economic security agreements with advanced industrial economies with strengths in robotics, like Japan, the European Union (especially Germany), and South Korea. The arrangements would focus on reducing trade barriers while also erecting complementary national security measures to block Chinese firms. - Restrict U.S. Outbound Investment in Chinese Robotics Companies. U.S. and allied venture capital funding has enabled the growth of China’s robotics ecosystem. For example, successful Chinese robotics startup Unitree received investment from a China-focused subsidiary of a U.S.-headquartered fund, but the company is now developing robotic systems for China’s military.[15] The United States should expand the recently issued rule restricting U.S. investment in AI, semiconductor, and quantum technology-related firms in countries of concern to include robotics.[16]

Conclusion

Securing U.S. leadership in AI and robotics is crucial for America’s economic competitiveness and national security. Through coordinated action across government, industry, and academia, the United States can build a robust domestic robotics ecosystem while accelerating adoption across critical sectors. Setting ambitious national goals, providing targeted financial incentives, and protecting against Chinese market distortions will help ensure American leadership in this transformative technology. By implementing these recommendations, the United States can create a future where robotics and AI drive productivity growth, strengthen our manufacturing base, and enhance our workforce capabilities. Success in this endeavor will require sustained commitment and investment, but the economic and strategic benefits of leadership in robotics and embodied AI make this effort essential to securing America’s technological future.

[1] 2.1 Million Manufacturing Jobs Could Go Unfilled By 2030, National Association of Manufacturers (2021).

[2] Record of 4 Million Robots in Factories Worldwide, International Federation of Robotics (2024); Alexander Brown, et al., Robotics sector + “Complete industrial chain” + Industrial internet, Mercator Institute for China Studies (2023).

[3] National Action Plan for United States Leadership in Advanced Manufacturing, Special Competitive Studies Project at 15-16 (2024).

[4] Will the United States or China Lead in Humanoid Robotics?, Special Competitive Studies Project (2024).

[5] Peter Haas, Tech Panel 2: The Shape of the Robotics Innovation Ecosystem, SCSP AI+ Robotics Summit at 10:30 (2024).

[6] Will the United States or China Lead in Humanoid Robotics?, Special Competitive Studies Project (2024).

[7] Towards Resilient Manufacturing Ecosystems Through Artificial Intelligence, National Institute of Standards and Technology at A-3, C-8 (2022).

[8] Elisabeth Reynolds, et al., Digital Technology and Supply Chain Resilience: A Call to Action to Accelerate U.S. Manufacturing Competitiveness, Massachusetts Business Roundtable & Manufacturing, MIT at 2 (2023).

[9] National Action Plan for United States Leadership in Advanced Manufacturing, Special Competitive Studies Project at 26 (2024).

[10] National Action Plan for United States Leadership in Advanced Manufacturing, Special Competitive Studies Project at 39 (2024).

[11] William B. Bonvillian, Restoring Leadership in U.S. Manufacturing, Day One Project at 4 (2020).

[12] ARM Institute Launches Job Matching Capabilities on RoboticsCareer.org, ARM Institute (2023); New Credential Engine & ARM Institute Partnership To Address Needs For Skills-Based Economy, Credential Engine (2022).

[13] Commerce Announces Proposed Rule to Secure Connected Vehicle Supply Chains from Foreign Adversary Threats, U.S. Department of Commerce, Bureau of Industry and Security (2024).

[14] ICT Supply Chain, U.S. Department of Commerce (last accessed 2024); Executive Order 13873, The White House (2019).

[15] Unitree Overview, PitchBook (last accessed 2024).

[16] Provisions Pertaining to U.S. Investments in Certain National Security Technologies and Products in Countries of Concern, U.S. Department of Treasury (2024).